| Close | Previous Close | Change | |

|---|---|---|---|

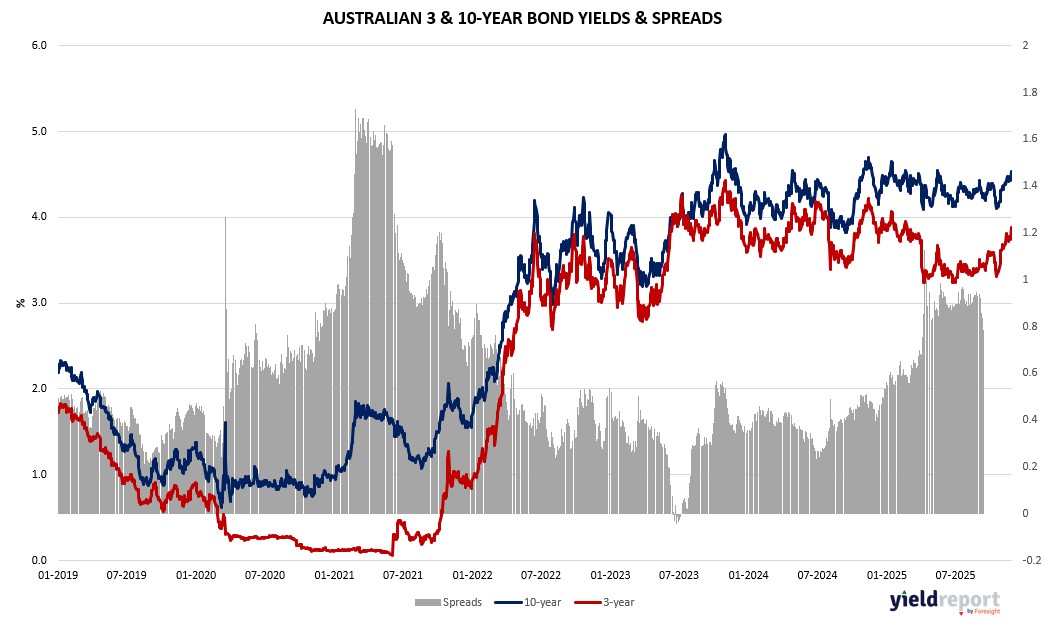

| Australian 3-year bond (%) | 3.882 | 3.742 | 0.14 |

| Australian 10-year bond (%) | 4.531 | 4.433 | 0.098 |

| Australian 30-year bond (%) | 5.11 | 5.06 | 0.05 |

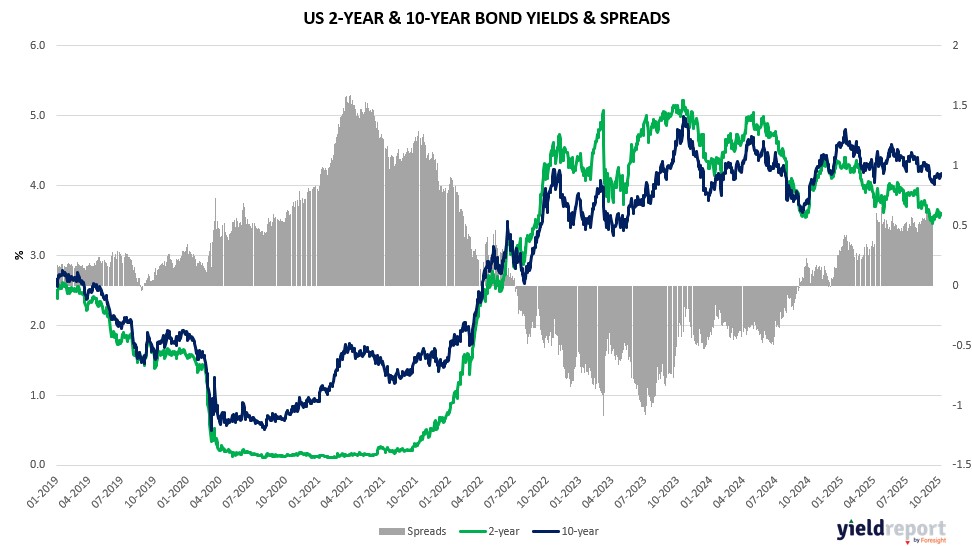

| United States 2-year bond (%) | 3.467 | 3.495 | -0.028 |

| United States 10-year bond (%) | 4.011 | 4.038 | -0.027 |

| United States 30-year bond (%) | 4.6619 | 4.6775 | -0.0156 |

Overview of the Australian Bond Market

Australian bond yields surged on November 26, 2025, after hotter October inflation data dashed rate-cut expectations and fueled bets on a Reserve Bank hike in 2026. The 10-year yield climbed six basis points to 4.48%, the 2-year rose 10 basis points to 3.77%, and the 5-year advanced 10 basis points to 4.02%, reflecting a reassessment of the RBA’s easing cycle amid persistent price pressures. The move widened the AU-US differential, supporting AUD/USD’s 0.75% rally to above its 200-day moving average, with next targets at 0.6580.

CPI accelerated to 3.8% year-on-year, exceeding the 3.6% forecast, while trimmed mean hit 3.3%, trending up since June and well above the RBA’s 2.5% midpoint. Non-tradables rose 4.8%, services 3.9%, underscoring domestic drivers like housing and rents. This contrasted with Fed cut odds at 80% for December, highlighting diverging policies that could sustain AUD upside if US data weakens next week, like ADP employment and ISM PMI.

The APRA’s new mortgage limits, capping debt-to-income over six times at 20% of new loans, aim to preempt risks from high indebtedness, as housing credit grows above average and prices surge. Building activity picked up, with residential work up 4.2% in Q3, signaling capacity strains that risk inflating further, per Citigroup economists noting growth nearing limits.

Markets now price a small 2026 hike chance, erasing cuts, with UBS eyeing Q4 2026 action and Barrenjoey warning of February moves to 3.85%. The RBA meets December 8-9, likely holding at 3.6% after August’s cut, as Assistant Governor Hunter flags labor tightness with unemployment at 4.3% and elevated wages.

Q3 capital expenditure due Thursday, forecast at +0.5%, could affirm strong GDP, complicating disinflation. Bloomberg Economics sees the inflation spike as transitory but needs more data to confirm. Yields may extend gains if momentum builds, though state policies could spur apartment supply late-decade, easing pressures.

Overview of the US Bond Market

Bond traders ramped up bets on a Federal Reserve rate cut in December following upbeat yet moderating economic data on November 26, 2025, pushing Treasury yields lower across the curve. The 10-year yield dipped two basis points to 4.00%, the 2-year fell one basis point to 3.47%, and the 30-year declined five basis points to 4.64%, flattening the 2s-10s curve by about two basis points. This came after a solid session where longer-dated bonds led gains, reflecting optimism that the Fed might ease further amid labor market slack and consumer caution, even as core inflation lingers.

The rally was fueled by jobless claims dropping to 216,000, a seven-month low, underscoring low layoffs but highlighting hiring reluctance tied to economic uncertainty and Trump’s policies. Continuing claims edged up to 1.960 million, a proxy for hiring, during the period surveyed for November’s unemployment rate, which could rise faster than implied given ineligible claimants like recent graduates. Durable goods orders rose 0.5%, with core shipments jumping 0.9%, signaling robust equipment spending driven by AI investments, though wild swings from tariffs have undercut manufacturing segments. Retail sales advanced just 0.2% in September, with control-group sales down 0.1%, suggesting softer fourth-quarter consumption but not derailing holiday outlooks from retailers like Kohl’s and Abercrombie.

Swap contracts now price in an 80% chance of a December cut, revived by weak private payrolls and subdued retail figures, contrasting with earlier divisions among Fed officials. Kevin Hassett’s potential as next Fed chair, seen as dovish, added to sentiment, though robust data like September’s producer price index up 0.3% tempers aggressive easing expectations. The Bloomberg Dollar Spot Index fell 0.3%, with the dollar steady against major currencies, as EUR/USD rose 0.2% and AUD/USD climbed 0.7% on Australia’s hot CPI.

JPMorgan’s weekly Treasury client survey showed net long positions shrinking to the smallest in two months, indicating reduced bullishness ahead of key releases. Asset managers pared longs across futures by $23.5 million per basis point, while leveraged funds reduced shorts in the bond contract. Dealers expect steady coupon auction sizes for August-October, aligning with April guidance.

Macro factors like tariffs continue to cloud the outlook; deals with allies have eased some uncertainty, but potential extensions with China—possibly by 90 days—could influence yields. With GDP forecasted at 3.9% for Q3, above potential, and consumer confidence sliding due to job anxieties, bonds may face pressure if growth overshoots, sustaining higher-for-longer rates. Yet, resilience in the face of shutdown delays and AI-driven spending supports a soft landing narrative, keeping yields range-bound as markets eye PCE inflation on December 5.