| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.738 | 3.781 | -0.043 |

| Australian 10-year bond (%) | 4.442 | 4.48 | -0.038 |

| Australian 30-year bond (%) | 5.048 | 5.071 | -0.023 |

| United States 2-year bond (%) | 3.57 | 3.598 | -0.028 |

| United States 10-year bond (%) | 4.104 | 4.127 | -0.023 |

| United States 30-year bond (%) | 4.715 | 4.7279 | -0.0129 |

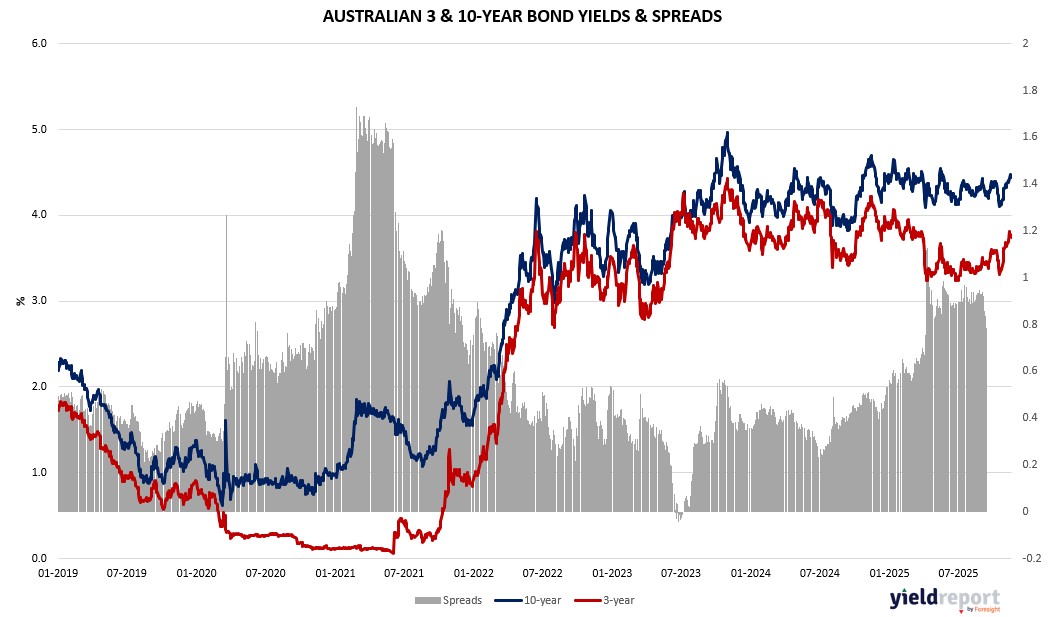

Overview of the Australian Bond Market

Australian government bond yields rose on November 19, 2025, tracking US Treasury weakness amid Fed hawkishness and dollar strength, with local data reinforcing stability but highlighting risks. The 10-year yield advanced five basis points to 4.46%, the 2-year rose three to 3.69%, the 5-year up three to 3.95%, the 15-year four to 4.77%. One-day changes were positive, with monthly gains from 31 to 44 basis points, though yearly shifts mixed from -40 to +3.

The uptick reflected APRA’s warnings on elevated overseas risks and persistent geopolitical volatility, eroding resilience if unprepared. Domestically, high household debt remains a vulnerability, with signs of rising higher-risk lending like high debt-to-income investor borrowing, despite sound overall standards. The regulator’s new biannual System Risk Outlook emphasizes stability but calls for stronger geopolitical risk management across institutions, varying in maturity.

Wage data aligned with expectations at +0.8% quarter-on-quarter and +3.4% year-on-year, signaling decent growth but slowing private momentum amid labor easing— a lagging indicator aiding consumer sentiment but underscoring caution. This blends with global macro uncertainty: Fed minutes leaned hawkish with steady 2025 rates and missing jobs data, pressuring yields higher as rate cut bets fade.

Investor sentiment ties to US crypto crash and Nvidia’s positive earnings countering AI spending fears, but Australia’s financial system acts as a stabilizer via super funds, per APRA’s stress test with major banks and funds. Structural features can amplify shocks on members, urging diversification.

Bond positioning may mirror US caution, with trimmed longs ahead of Fed clarity. Upcoming flash PMIs on November 20 could sway, with Manufacturing and Services forecasts vs priors. China’s unchanged LPR and US CPI (Core 0.3% month-on-month) add layers.

Overall, yields remain elevated on resilience narratives, but strategists advise watching tariffs and geopolitics, echoing UBS’s confidence in AI-driven equities despite pullbacks.

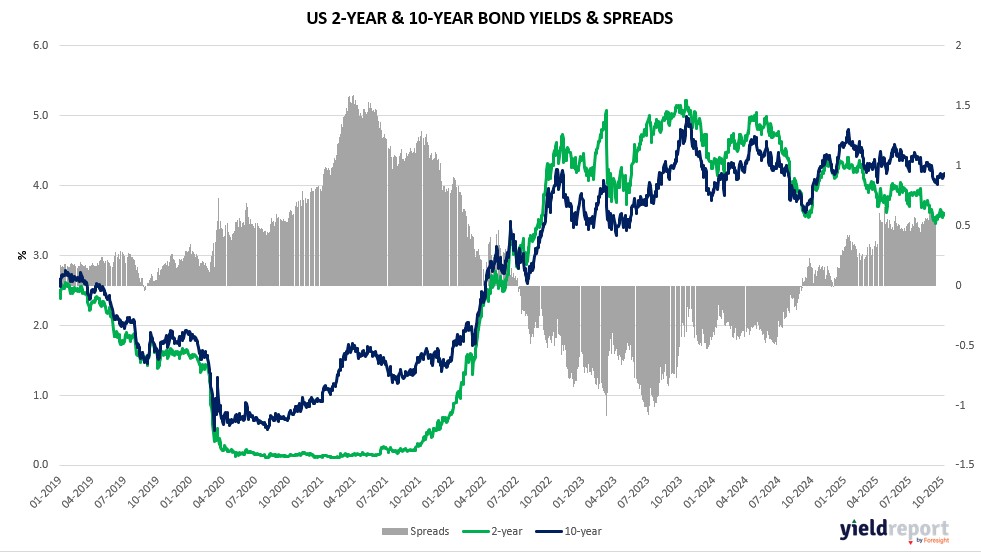

Overview of the US Bond Market

Bond yields rose across the curve on November 19, 2025, as Treasuries fell amid hawkish Fed signals and a strengthening dollar, reducing bets on imminent rate cuts. The 10-year yield climbed two basis points to 4.14%, while the 2-year advanced 13 basis points to 3.59%, and the 30-year rose 15 basis points to 4.76%. Shorter maturities saw gains too: 3-month at 3.78% (up 3.87%), 6-month at 3.70% (up 3.82%), and 12-month at 3.52% (up 3.66%). The moves reflected minutes from the Fed’s October meeting, where officials indicated steady rates through 2025, with uncertainty from missing October jobs data—incorporated into November’s report post the year’s final meeting. Traders nearly eliminated expectations for a December cut, bolstering the dollar’s 0.5% gain.

Macro uncertainty looms large, with geopolitical tensions, inflation persistence, and tariff impacts clouding the outlook. Fed Chair Jerome Powell faces potential dissent, but the minutes leaned hawkish, as TradeStation’s David Russell noted, with policymakers “flying blind” amid lost data and unclear tariff effects. This resilience in the US economy, despite crypto turmoil and tech volatility, supports views that rates may stay higher longer, pressuring bond prices. Oil’s decline on inventory builds added to commodity weakness, though gold’s second-day climb offered a safe-haven counter.

Investor positioning shifted cautiously: asset managers trimmed net long Treasury futures by $23.5 million per basis point in recent CFTC data, focused on 5-year and classic bonds, while leveraged funds reduced shorts. JPMorgan’s survey showed net longs at a two-month low ahead of the Fed meeting, signaling less bullish sentiment despite steady policy expectations—swap contracts price under half a point of easing by year-end.

The bond market’s reaction ties into broader narratives: Nvidia’s robust earnings eased AI spending fears, but stretched valuations and dimming rate relief keep yields elevated. Treasury Secretary comments on ongoing US-China talks for tariff truce extensions were absent, but similar past deals with the EU suggest limited market spurs. Economic data showed consumer confidence holding, but job concerns linger, with upcoming releases like Core CPI (forecast 0.3% month-on-month) and Retail Sales (0.4%) on November 20 poised to influence.

Dealers expect steady coupon auction sizes for August-October, per April guidance, with 10- and 5-year potentially up $1 billion. Australia’s regulator warnings on high household debt echo global vulnerabilities, amplifying focus on geopolitical risks that APRA sees as heightened and persistent.

Overall, bonds remain sensitive to Fed clarity, with strategists from HSBC, Morgan Stanley, and UBS eyeing long-term equity upside from earnings and AI, but advising diversification amid high valuations and potential tariff bites.