| Close | Previous Close | Change | |

|---|---|---|---|

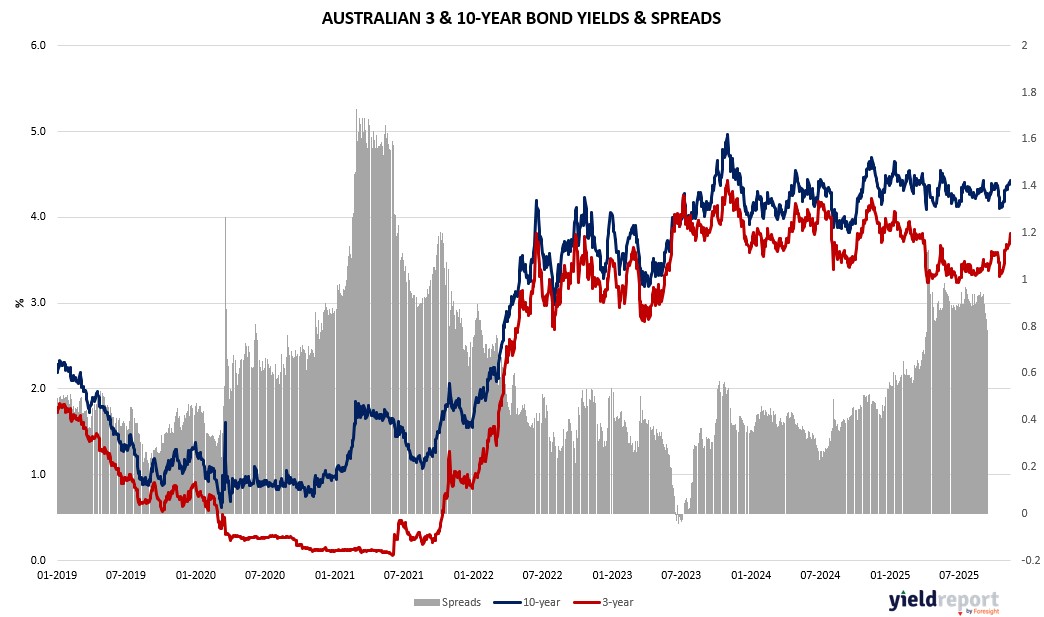

| Australian 3-year bond (%) | 3.761 | 3.807 | -0.046 |

| Australian 10-year bond (%) | 4.435 | 4.427 | 0.008 |

| Australian 30-year bond (%) | 5.034 | 5.007 | 0.027 |

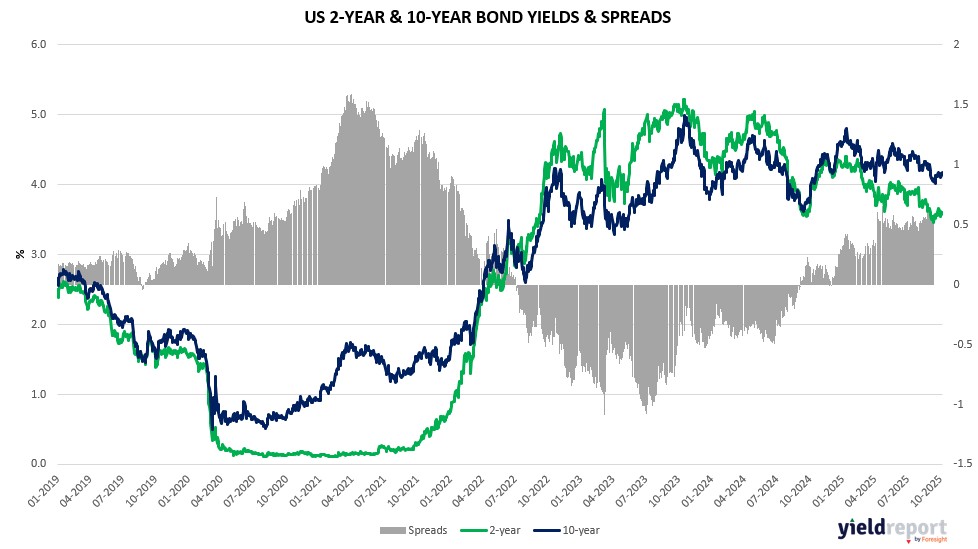

| United States 2-year bond (%) | 3.589 | 3.593 | -0.004 |

| United States 10-year bond (%) | 4.125 | 4.096 | 0.029 |

| United States 30-year bond (%) | 4.7229 | 4.6782 | 0.0447 |

Overview of the Australian Bond Market

Australian government bond yields dipped slightly on November 14, 2025, bucking US rises as local risk aversion deepened, with 10-year down two basis points to 4.43%, 2-year four to 3.68%, 5-year one to 3.94%, 15-year two to 4.73%. This reflected global Fed angst—December odds 50/50 per CME—amid Schmid’s inflation warnings beyond tariffs, potentially crisis per Guha, though data like September retail (0.6% vs 0.4% poll), October core CPI (0.3% match) could clarify cuts if benign. Blended macro: Trump’s food tariff cuts—beef +13% YOY—retroactive via Latin pacts, $2,000 dividends eyed, address affordability post-elections, but Democrats slam as self-made.

Bond moves amid ASX rout—tech -4.42%, financials -1.86%—on October jobs resilience, no RBA easing. China’s AI shift to power, metals per BofA—1/3 spend infrastructure, copper +20% demand—lifts utilities (CSI energy P/E 13 vs IT 34), CATL high on storage. UBS’s Ken Liu favours power equipment on 8% demand growth by 2028.

Corporate allure: Google $40B Texas centres, solar co-located; Anthropic $50B US plans. Oracle CDS surge on AI debt. Dealers’ steady auctions. Opposition ditches net zero, Bowen pushes COP31. Overall, bonds drew mild safety amid volatility, data resumption key—September nonfarms (22k vs 50k) eyed, per TD’s Goldberg contentious Fed.

Overview of the US Bond Market