| Close | Previous Close | Change | |

|---|---|---|---|

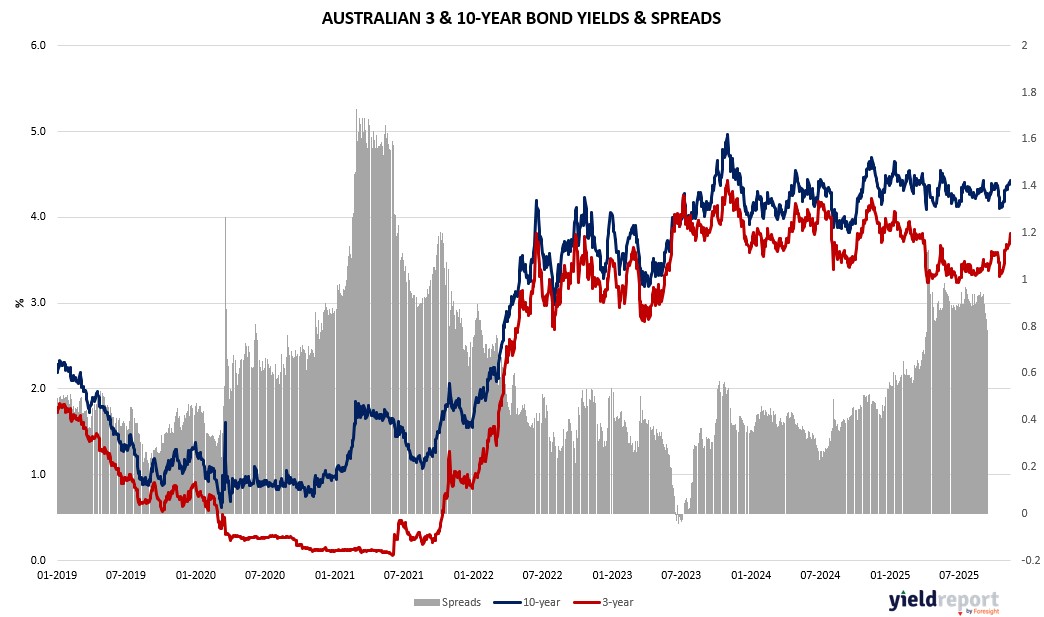

| Australian 3-year bond (%) | 3.807 | 3.7 | 0.107 |

| Australian 10-year bond (%) | 4.427 | 4.383 | 0.044 |

| Australian 30-year bond (%) | 5.007 | 4.992 | 0.015 |

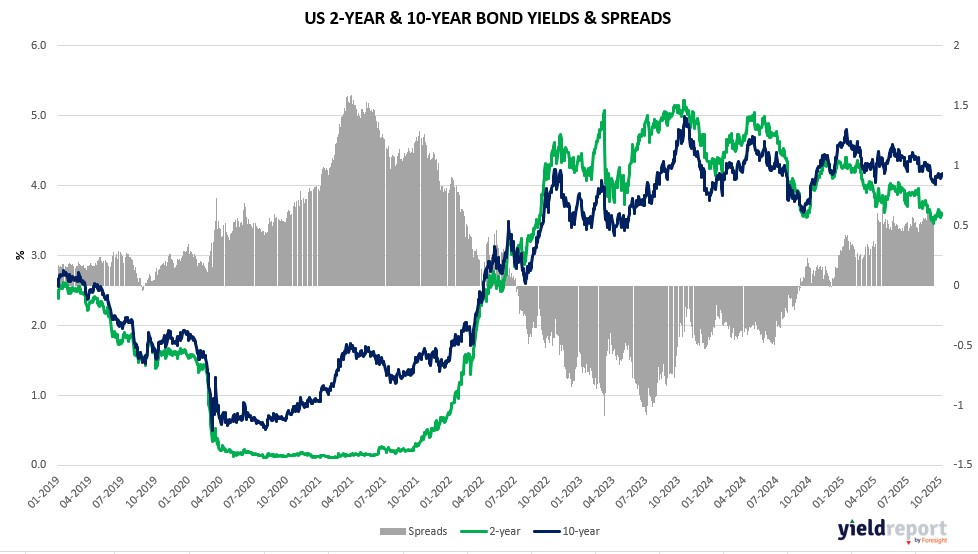

| United States 2-year bond (%) | 3.593 | 3.564 | 0.029 |

| United States 10-year bond (%) | 4.096 | 4.089 | 0.007 |

| United States 30-year bond (%) | 4.6782 | 4.6898 | -0.0116 |

Overview of the Australian Bond Market

Australian government bond yields surged on November 13, 2025, mirroring US climbs as robust October jobs—unemployment 4.3% vs 4.4% forecast, +42.2k employed—cemented no near-term RBA cuts, with 10-year up eight basis points to 4.45%, 2-year ten to 3.73%, 5-year eleven to 3.96%, and 15-year seven to 4.75%. This dashed December easing hopes, affirming RBA’s tight economy stance per BetaShares’ David Bassanese—cuts next year need inflation relief or weakening, despite annual employment growth slowing to 1.6% per EY’s Cherelle Murphy.

US data torrent post-shutdown fueling global caution, with incomplete October jobs skipping unemployment per Hassett, complicating Fed’s December odds below 50% amid officials’ divides—Musalem against inflation, Hammack restrictive, Kashkari opposing prior cut. Private glimpses like ADP’s 11k shed, Indeed’s 16% retail drop hint pressures, but Apollo’s Slok flagged 55% CPI items over 3%, mirroring AU resilience. Treasury Secretary Bessent’s tariff tweaks for coffee, bananas to cut prices—targeting non-US goods—echo Trump’s affordability push via domestic travel, rebates discussion, amid election losses tied to living costs.

Corporate bonds appeal grows, with lower yields for Microsoft, Siemens vs sovereigns as G7 debt rises, firms deleverage to 1.74x EBITDA. MFS’s Gomez-Bravo cited fiscal erosion, TD’s Mikkelsen government spending vs profits. Upgrades fastest in decade, Meta/Alphabet bids massive despite AI jitters.

Flows reflect rotations, materials +1.71% on lithium/gold, but tech -3.92%, real estate -2.78% yield-sensitive. Opposition ditching net zero by 2050 per Ley adds policy uncertainty. RBA’s Michelle McPhee fireside Friday eyed. Overall, bonds sold off on jobs beat, though data resumption could sway if benign, per BDO’s Magnusson—September US retail (0.4% forecast) key.

Overview of the US Bond Market

Treasury yields climbed on November 13, 2025, reversing prior declines as divided Fed signals on rates and shutdown aftermath stoked inflation fears, with 10-year yields up five basis points to 4.12%, 2-year three to 3.60%, and 30-year five to 4.71%. The move reflected eroding bets on December easing—now below 50%—amid hawkish tones from officials like Musalem leaning against inflation with limited room to cut, Hammack advocating restrictiveness, and Kashkari opposing October’s move. This, blended with macro uncertainty from delayed data like September’s nonfarm payrolls (50k forecast) and incomplete October jobs skipping unemployment per Hassett, suggested policymakers may pause to parse signals, per Evercore’s Krishna Guha.

Bond traders positioned for volatility, with BMO’s Ian Lyngen noting private data’s resilience could bolster hold-steady cases if labor softens less than feared. Weekly jobless claims at 225k forecast for November 8 aligned with stability, but ADP’s 11k job shed and Indeed’s 16% retail posting drop hinted pressures. Apollo’s Torsten Slok flagged 55% of CPI items rising over 3%, complicating cuts. Treasury Secretary Scott Bessent’s “substantial” tariff tweaks for coffee, bananas to lower prices—echoing Trump’s Fox comments—added disinflation hopes, though no $2,000 rebate decisions. Trump’s domestic travel to tout affordability, per sources, signals focus on living costs post-election losses tied to tariffs.

Corporate bonds drew appeal, with investors demanding lower yields for Microsoft, Airbus than sovereigns, per Bloomberg data, as G7 debt-to-GDP rises to 137% by 2030 per IMF, versus leaner firm leverage at 1.74x EBITDA. MFS’s Pilar Gomez-Bravo cited eroding rule-of-law perceptions, shifting regimes favor corporates. TD’s Hans Mikkelsen contrasted government reelection spending with profit-driven firms. Upgrades outpace downgrades at decade highs, with Meta, Alphabet drawing massive bids despite AI spend jitters.

Asset managers pared longs in futures by $23.5m per bp, focused on 5- and 30-year, while leveraged trimmed shorts. Dealers expect steady auctions August-October. BCA’s Mathieu Savary noted profligate policies in US, Japan give comfort but overblown fiscal concerns for powerful nations. Overall, bonds faced pressure from rate-pause bets, though data resumption could sway if revealing benign inflation or softening jobs, per Capital Economics’ Thomas Ryan—survey delays mean weeks for full picture, Thanksgiving complicating November.