| Close | Previous Close | Change | |

|---|---|---|---|

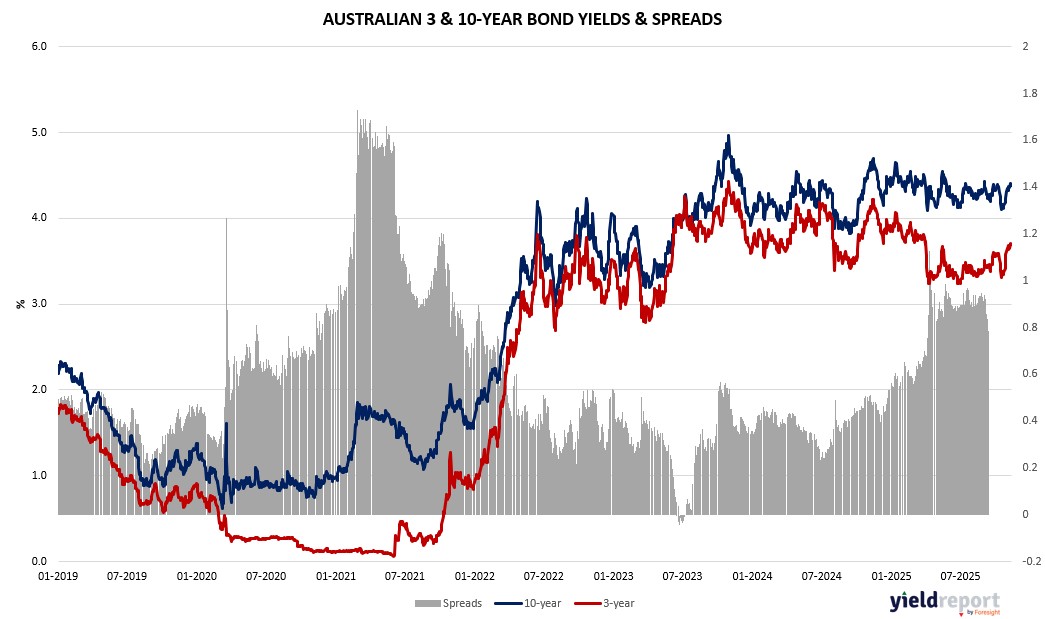

| Australian 3-year bond (%) | 3.7 | 3.708 | -0.008 |

| Australian 10-year bond (%) | 4.383 | 4.396 | -0.013 |

| Australian 30-year bond (%) | 4.992 | 5.01 | -0.018 |

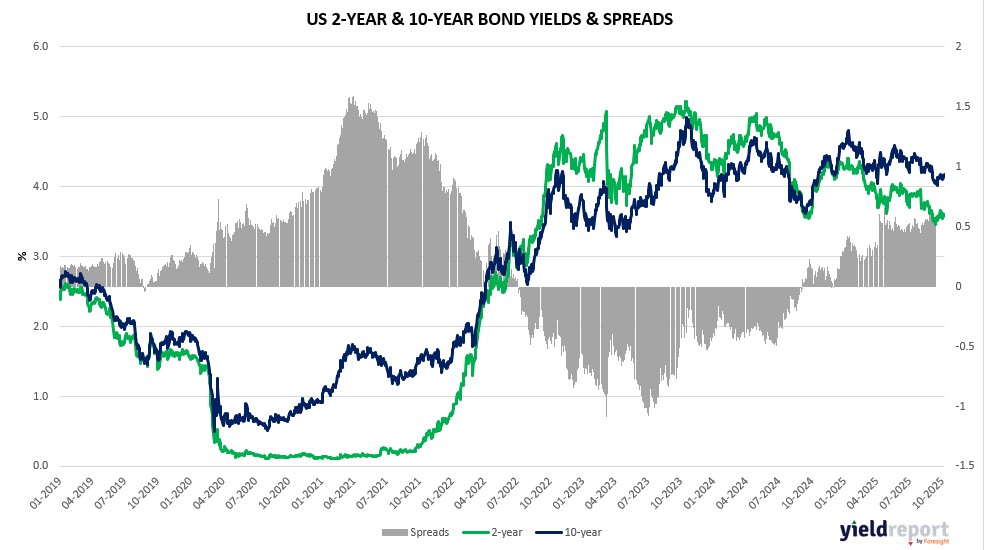

| United States 2-year bond (%) | 3.564 | 3.591 | -0.027 |

| United States 10-year bond (%) | 4.089 | 4.11 | -0.021 |

| United States 30-year bond (%) | 4.6898 | 4.702 | -0.0122 |

Overview of the Australian Bond Market

Australian government bonds saw yields ease slightly on November 12, 2025, tracking US Treasuries lower amid global bets on Fed easing post-shutdown, with the 10-year yield little changed at 4.38% after dipping two basis points intraday. The 2-year fell one to 3.62%, 5-year one to 3.85%, and 15-year three to 4.67%, reflecting cautious positioning ahead of local jobs data and US data resumption. This supports a soft landing narrative, though RBA cuts remain distant, with markets pricing no move until mid-2026 amid persistent inflation.

US shutdown end boosting sentiment, as delayed September data like nonfarm payrolls (50k forecast) and CPI could clarify Fed path, potentially two cuts by early 2026 per UBS, aiding global bonds. Locally, October employment eyed at +20.3k, unemployment 4.4%, per polls—stable labor may keep RBA hawkish, but tariff talks add disinflation hopes. Treasury Secretary Bessent’s signals on cutting US tariffs for coffee, bananas signal broader relief, echoing Trump’s Fox comments, which could ease import costs Down Under.

Bond flows reflect rotation, with resources up on China stimulus whispers—iron ore gains supporting AUD stability at $0.6528. Yet, tech rout (-3.3%) highlights risk-off, favoring defensives like staples (+1.05%). Economic voids from US shutdown mirror local concerns; CBO’s $7-14bn unrecovered GDP hit underscores drags, though Vanguard sees temporary. Private data suggests polarized economy—AI thriving, tariffs hurting—per economists, confusing post-shutdown floods like September retail sales (0.4% forecast).

Dealers expect steady auction sizes, aligning with US views. Yen warnings from Japan add currency volatility, with AUD unchanged. Overall, bonds drew safety bids amid equity wobbles, with shutdown resolution poised to lift fog, though repricing if data surprises strong.

Overview of the US Bond Market

Treasuries rallied on November 12, 2025, with yields falling across the curve as traders piled into options betting on a 10-year drop below 4%, fueled by expectations of a Federal Reserve rate cut in December to support the jobs market amid shutdown-induced data delays. The 10-year yield slid five basis points to 4.07%, the 2-year declined three to 3.56%, and the 30-year fell four to 4.66%. This extended a bond-friendly backdrop, with the rally gaining steam ahead of the House vote to end the 43-day shutdown, unlocking delayed economic indicators like September’s nonfarm payrolls and CPI, though October data may remain lost, per White House statements.

Bond traders adjusted positions cautiously, with JPMorgan’s client survey showing net longs shrinking to two-month lows, reflecting tempered bullishness despite steady Fed easing bets—swap contracts pricing just under 50 basis points by year-end. The resilience of the US economy, even sans official data, bolsters views that rates may stay higher longer, but shutdown resolution could clarify the outlook, potentially reinforcing cuts if labor softens. Seema Shah at Principal Asset Management highlighted the difficulty in assessing growth without reports, yet anticipates a re-emerging December cut case, favoring risk assets.

Oil plunged 4.3% on supply concerns easing inflation fears, while gold and copper advanced on dovish Fed wagers. Treasury Secretary Scott Bessent’s comments on “substantial” moves to cut prices of imports like coffee and bananas—via potential tariff tweaks—added to disinflation hopes, though no decisions on $2,000 rebates. Trump’s tariff truce talks with China, set to expire soon, could extend 90 days, per Bessent, mirroring EU deals that tempered market reactions but supported bonds by dissipating uncertainty.

Economic glimpses from private sources suggest stable labor—weekly jobless claims at 225,000 forecast for November 8—aligning with Vanguard’s Josh Hirt viewing shutdown effects as temporary, with Q4 GDP drag offset in Q1 2026. Yet, the K-shaped economy, per Fundstrat’s Hardika Singh, with tech thriving on AI and others lagging tariffs, may confuse post-shutdown data floods, including delayed September industrial production (0% forecast) and retail sales (0.4%). UBS’s Ulrike Hoffmann-Burchardi expects two more cuts by early 2026, aiding equities, bonds, and gold.

Primary dealers anticipate steady coupon auction sizes for August-October, per surveys, with high-grade bond sales hitting 2020 highs. Asset managers pared net longs in futures by $23.5 million per basis point, focused on 5- and 30-year, while leveraged funds trimmed shorts. Atlanta Fed President Raphael Bostic’s retirement announcement added policy intrigue. Overall, bonds benefited from shutdown end bets and rate-cut positioning, though repricing risks loom if resumed data surprises, per TD Securities’ Oscar Munoz.