| Close | Previous Close | Change | |

|---|---|---|---|

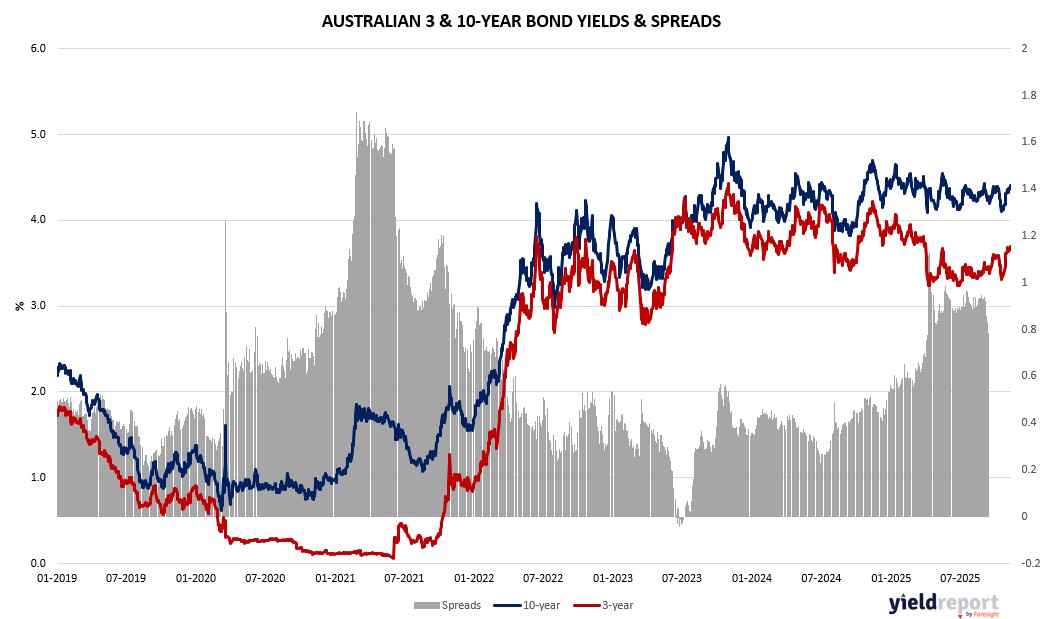

| Australian 3-year bond (%) | 3.708 | 3.697 | 0.011 |

| Australian 10-year bond (%) | 4.396 | 4.405 | -0.009 |

| Australian 30-year bond (%) | 5.01 | 5.027 | -0.017 |

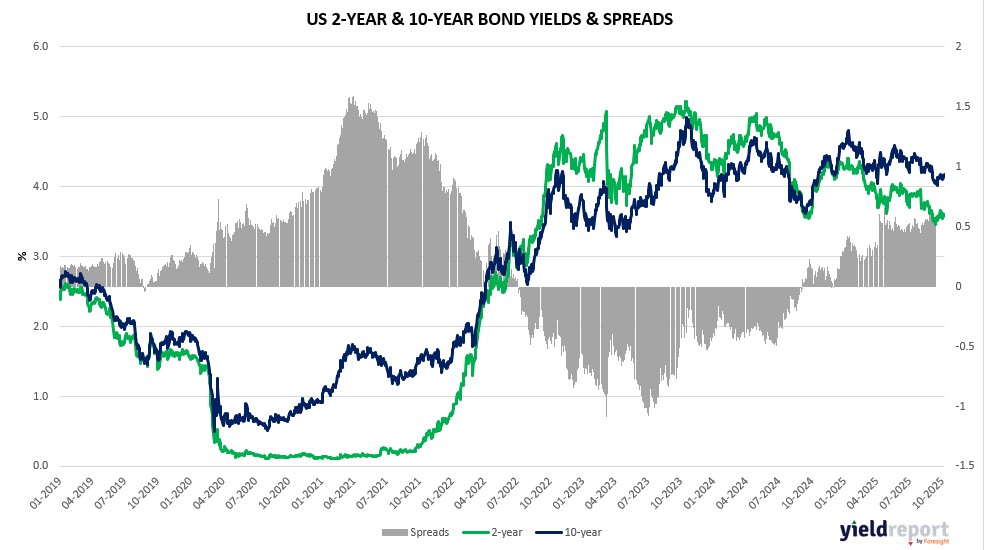

| United States 2-year bond (%) | 3.591 | 3.597 | -0.006 |

| United States 10-year bond (%) | 4.11 | 4.132 | -0.022 |

| United States 30-year bond (%) | 4.702 | 4.7299 | -0.0279 |

Overview of the Australian Bond Market

Australian government bonds firmed slightly on November 11, 2025, with yields edging lower amid US shutdown progress and domestic data signaling economic resilience. The 10-year yield fell 3 basis points to 4.36%, the 2-year unchanged at 3.62%, and the 15-year down 3 to 4.67%. Trading reflected caution ahead of key releases, with investors eyeing potential RBA hold amid improving sentiment.

Westpac’s consumer index hit 103.8, a 44-month high, and NAB’s business conditions rose to 9, underscoring recovery per AMP’s My Bui, though labor softening raises questions. Capacity at 83.4% flags inflation, likely delaying RBA cuts. Globally, US reopening optimism boosted risk appetite, but delayed data like September non-farm payrolls (+50k forecast November 14) and October CPI (+0.3% core m/m November 20) could inject volatility, influencing Fed paths and AUD flows.

Positioning shows mixed bets: Reuters notes AUD/USD paused at 0.6516-0.6537 on US yield gains, but gold lifts and USD/CNH retreats aided recovery. Bulls eye monthly wick and DMA holds, though RSIs and cloud resistance concern longs. Broader macro ties to US: Senate bill advances, House vote Wednesday, per Bloomberg, with post-shutdown GDP rebound estimated 0.4-1% Q4 hit but quick bounce.

Strategists like Investec’s Philip Shaw see data deluge as a “huge market event,” aligning Fed and economy views. UBP’s Carlos Casanova highlights rebound pricing. In commodities, gold’s rise supports haven demand, copper up 0.5%, Brent down 0.25%. Betashares reported minor short sales in green bonds, signaling low conviction.

With China’s data Friday (industrial +5.5%, retail +2.8%) and AU employment November 13 (+20.3k, 4.4% unemployment), bonds may see pressure if growth strengthens. RBA’s steady stance amid home prices at 15-year highs contrasts Fed cut bets, but tariff risks from Trump linger, per Treasury’s Bessent on China truce talks. Overall, yields reflect balanced outlook, with diversification urged amid AI-driven equity highs.

Overview of the US Bond Market

Bond trading was subdued on November 11, 2025, with the US Treasury market closed for Veterans Day, but futures advanced as investors positioned for the government shutdown’s end and a flood of delayed economic data. Treasury futures rose, with the 10-year note contract up 33 basis points to 113.02%, reflecting bets on renewed data clarity influencing Federal Reserve decisions. Yields on cash Treasuries, last quoted Friday, showed the 10-year at 4.12%, down from recent peaks, amid expectations for labor and inflation figures to shape rate-cut probabilities.

The shutdown’s resolution, with the Senate passing a funding bill and the House poised to act Wednesday, has traders anticipating releases like September’s non-farm payrolls (forecast +50k) on November 14, industrial production on November 10, and October core CPI (+0.3% m/m) on November 20. Private indicators, such as ADP’s labor slowdown, have filled the void, bolstering cases for Fed easing. Swap markets price in potential December cuts, though Chair Jerome Powell’s recent caution underscores data dependency.

Positioning data reveals caution: JPMorgan’s client survey showed net longs shrinking to two-month lows, with asset managers trimming $23.5 million per basis point across tenors in CFTC data through July 22—wait, recent flows indicate reduced longs in 5-year and bond contracts, while leveraged funds pared shorts. This reflects crosscurrents—resilient economy versus shutdown disruptions—amid Trump’s tariff policies, though deals with allies have eased some uncertainty.

Strategists like Cameron Crise at Bloomberg note Nvidia’s November 19 earnings as a risk, but emphasize data resumption could affirm GDP rebound, per UBP’s Carlos Casanova estimating 0.4-1% Q4 hit with post-shutdown bounce. Dealers expect steady coupon auction sizes for August-October, signaling Treasury’s confidence. Oil’s 1.3% rise to $60.92 supported inflation hedges, while gold climbed 0.3% to $4,128.45, underscoring safe-haven demand.

Broader macro views remain constructive: HSBC, Morgan Stanley, and UBS hold bullish outlooks on earnings and AI tailwinds, even as valuations stretch. Yet, Goldman Sachs warns tariffs could pressure equities and bonds if unresolved, advocating diversification. With the dollar little changed and euro up 0.2%, bonds may see volatility from upcoming jobless claims (November 13, +225k forecast) and retail sales data, testing the Fed’s higher-for-longer stance in a slowing labor market.