| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.751 | 3.761 | -0.01 |

| Australian 10-year bond (%) | 4.456 | 4.468 | -0.012 |

| Australian 30-year bond (%) | 5.107 | 5.103 | 0.004 |

| United States 2-year bond (%) | 3.522 | 3.503 | 0.019 |

| United States 10-year bond (%) | 4.067 | 4.056 | 0.011 |

| United States 30-year bond (%) | 4.711 | 4.6992 | 0.0118 |

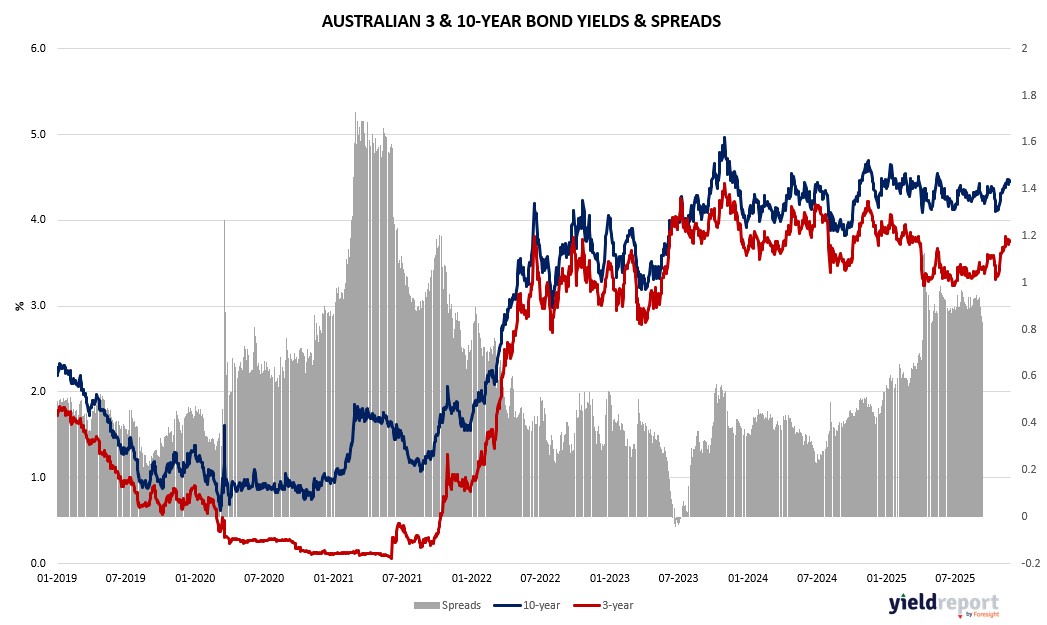

Overview of the Australian Bond Market

Australian government bond yields eased on November 24, 2025, mirroring US Treasuries amid tech-led equity rebounds and heightened global easing expectations. The 10-year yield fell 3 basis points to 4.43%, the 5-year dipped 2 basis points to 3.92%, the 2-year to 3.67%, and the 15-year to 4.74%. The 2s-10s curve steepened to +76 basis points, reflecting growth resilience but dovish tilts as Fed cut odds hit 85%.

The move tracked Wall Street’s surge, where Waller’s December cut support aligned with Australia’s upcoming data: October CPI Thursday at 3.6% year-over-year could affirm RBA vigilance on wages, blending into global inflation views. Q3 capital expenditure Wednesday at 0.5% might signal capex moderation, echoing US durable goods at 0.3%, potentially justifying holds amid consumer squeezes.

Geopolitically, BHP’s rebuffed Anglo bid—valuing it above £30/share—highlights copper consolidation risks, but Teck deal’s synergies could ease supply inflation. Trump-Xi call on truce extensions, soybeans, fentanyl added trade optimism, potentially capping yields via commodity flows. Ukraine peace framework refinements with US-Kyiv talks hint resolution, dovetailing Russia’s drone intercepts.

Dealers expect steady issuance, but macro integrates: resilient PMIs contrast jobs, with Westpac noting global activity. UBS strategists bull on earnings, but Weekly Economic Commentary warns volatility. Yields’ dip signals policy alignment, but G20 tensions and lithium weakness keep elevated, with GDP revisions Thursday key for Q3 assessments.

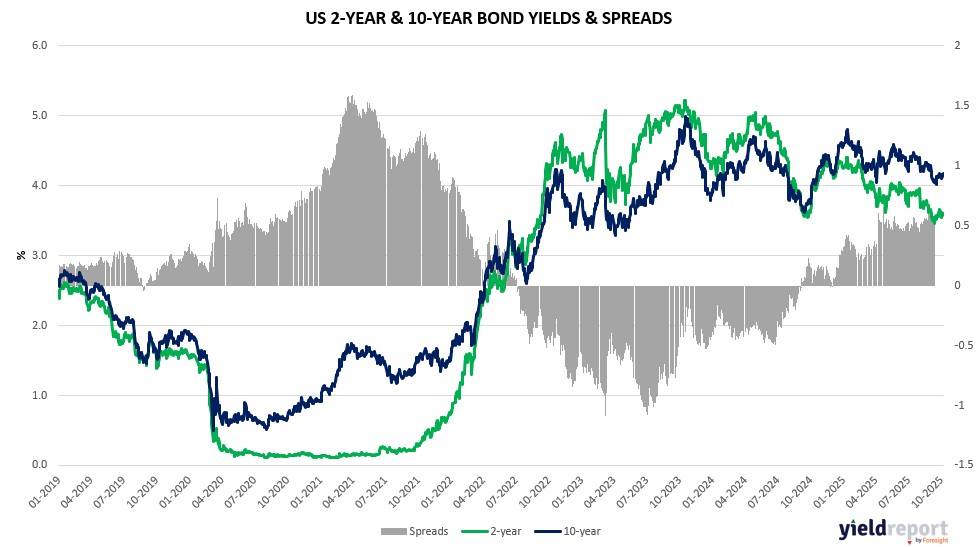

Overview of the US Bond Market

Bond traders ramped up Federal Reserve easing bets on November 24, 2025, following dovish comments from Governor Christopher Waller, sending Treasury yields lower to start the holiday-shortened week. The 10-year note yield fell 4 basis points to 4.02%, the 2-year dipped 1 basis point to 3.50%, and the 30-year eased 4 basis points to 4.67%. The 2s-10s curve flattened slightly to +52 basis points, signaling tempered growth expectations amid labor market signals and persistent inflation from delayed data.

The decline built on Friday’s momentum, where Williams’ remarks flipped December cut odds to over 85%, aligning with Waller’s support for easing to protect jobs. September retail sales, due Tuesday and projected up 0.4% month-over-month, could affirm consumer resilience but highlight squeezes from high prices, blending into Fed views on spending-driven growth. PPI for September, also Tuesday, might underscore manufacturing pressures, while durable goods orders expected at 0.3% could reflect industrial slowdowns echoing Australia’s Q3 capital expenditure at 0.5%.

Geopolitically, Trump-Xi talks on trade truce extensions—potentially 90 days per Bessent—eased supply inflation fears, but Taiwan tensions and Japan’s spat with China added uncertainty, potentially pressuring yields via safe-haven flows. San Francisco’s Daly backed a December cut, contrasting hawks like Cleveland’s Hammack warning of stability risks from over-easing amid tight spreads.

JPMorgan’s survey showed longs shrinking, with asset managers paring positions across tenors, while leveraged funds trimmed shorts. Dealers anticipate steady August-October auctions, but macro crosswinds loom: consumer confidence Tuesday at 93.4 could signal sentiment amid layoff announcements, dovetailing Australia’s October CPI at 3.6% year-over-year, hinting global price stickiness.

Oil rose 1.7% to $59.02 on Ukraine peace hopes, capping inflation, while gold climbed 1.6% to $4130.78 as havens. Bitcoin’s 1.2% gain to $88996 reflected risk rebound, but Reuters’ McGeever noted equity slumps could invoke Fed intervention for stability, given wealth effects on consumption—top 10% driving 35-50% per estimates. EUR/USD steady at 1.1522 amid ECB vigilance. Yields’ dip underscores policy recalibration, but G20 fissures and BHP’s Anglo bid highlight commodity volatility, with PCE Thursday pivotal for Q3 GDP revisions.