| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.761 | 3.774 | -0.013 |

| Australian 10-year bond (%) | 4.468 | 4.471 | -0.003 |

| Australian 30-year bond (%) | 5.103 | 5.082 | 0.021 |

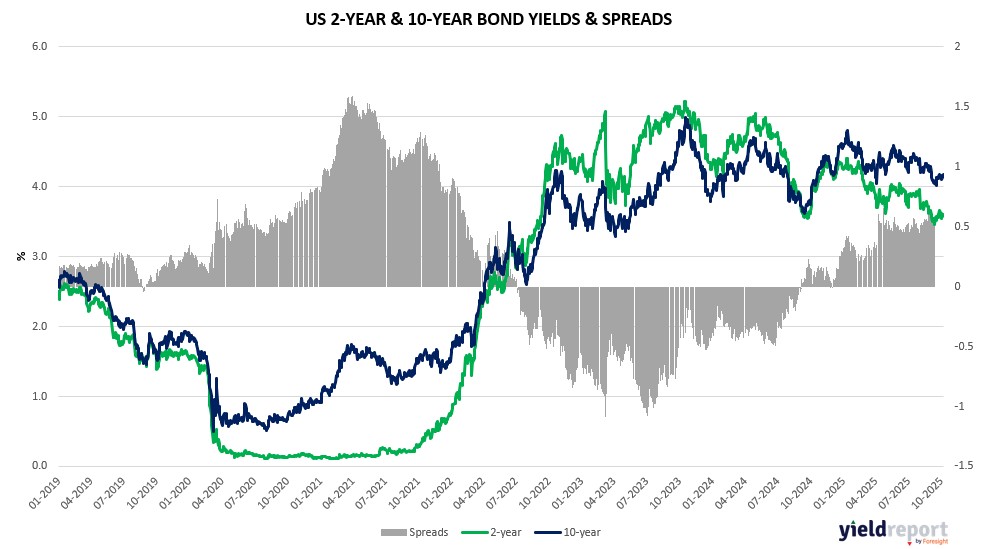

| United States 2-year bond (%) | 3,503 | 3.6 | 3499.4 |

| United States 10-year bond (%) | 4.056 | 4.133 | -0.077 |

| United States 30-year bond (%) | 4.6992 | 4.7468 | -0.0476 |

Overview of the Australian Bond Market

Australian government bond yields dipped modestly on November 21, 2025, tracking US Treasuries lower amid rebounding equities and recalibrated global rate bets. The 10-year yield edged down to 4.46%, the 5-year to 3.94%, the 2-year to 3.68%, and the 15-year held at 4.77%. Curve dynamics showed mild steepening, with 2s-10s at +78 basis points, reflecting growth resilience but dovish central bank tilts after mixed US data.

The move echoed Wall Street’s Friday rally, where Williams’ cut hints overshadowed September’s 119,000 payrolls and 4.4% unemployment, boosting AUD/USD 0.20%. Local Q3 wages rose 0.8% quarterly, aligning with RBA’s inflation vigilance, while flash PMIs signaled expansion—manufacturing at 51.6 diffusion index—bolstering case for steady rates. Yet, global AI despeculation and crypto plunge amplified risk aversion, drawing safe-haven bids into bonds.

Geopolitically, G20’s climate-focused declaration sans US input, amid Trump’s South Africa boycott, highlights multilateral strains that could fuel tariff risks, pressuring yields via trade channels. Modi’s Albanese meet emphasized critical minerals and energy ties, potentially easing supply inflation but underscoring dependencies. Japan’s stimulus package strained its yields, indirectly supporting AUD crosses.

RBA faces crosswinds: persistent wages echo US core CPI at 0.3%, tempering cuts, but consumer sentiment slumps and delayed US retail sales loom as Black Friday tests spending. Oil’s drop on Ukraine hopes eased pressures, while gold’s gain reflected havens. EUR/USD’s slip amid ECB’s Muller on 2% inflation vigilance added cross-currency flows.

Dealers anticipate steady issuance, but macro blends in: resilient PMIs contrast labor slowdowns, with Oxford’s Pearce noting employment risks to holidays. UBS strategists maintain bull views on earnings, but IG’s Sycamore warns post-peak sinister turns. Yields’ dip signals recalibration, but G20 fissures and tariff truces—Bessent on China extensions—keep volatility high, with upcoming durable goods pivotal for global demand.

and 10-year (blue) bond yields alongside the grey shaded area representing yield spreads from 2019 to 2025")

Overview of the US Bond Market

Bond traders boosted bets on Federal Reserve easing after New York Fed President John Williams signaled potential near-term cuts without inflation risks, sending Treasury yields lower on November 21, 2025. The 10-year note yield fell 8 basis points to 4.06%, the 2-year dropped 11 basis points to 3.51%, and the 30-year eased 5 basis points to 4.71%. The curve steepened slightly to +55 basis points in 2s-10s, reflecting growth optimism tempered by policy support expectations. A solid $44 billion 7-year auction met strong demand, with yields awarded at 3.85%, below expectations, underscoring haven flows amid equity volatility.

The move reversed part of Thursday’s yield spike tied to a risk-off cascade from crypto and AI stocks, where the VIX hit April highs. September jobs data showed 119,000 added payrolls and 4.4% unemployment, initially pushing December cut odds below 40% before Williams’ dovish tone flipped them to 70% via CME FedWatch. Core CPI at 0.3% month-over-month met forecasts, but persistent wage pressures from Australia’s data echoed global concerns, blending into US views on labor resilience. Philly Fed business index disappointed at -1.7 versus 2 expected, while existing home sales edged up to 4.1 million, signaling housing stability but no boom.

Geopolitically, Trump’s H200 chip float to China as a tariff compromise added uncertainty, with Bessent confirming ongoing talks on rare-earths and a potential 90-day truce extension—factors that could ease supply-chain inflation but risk hawkish backlash. Boston Fed’s Susan Collins and Dallas’ Lorie Logan urged steady rates, highlighting internal debate ahead of December’s meeting. JPMorgan’s client survey showed net longs shrinking to two-month lows, with asset managers paring $23.5 million per basis point across tenors, concentrated in 5s and bonds, while leveraged funds trimmed shorts.

Primary dealers expect steady coupon sizes for August-October auctions, aligning with April guidance, but macro crosscurrents cloud the outlook: resilient consumer confidence from Michigan’s 51.0 reading contrasts slowing jobs, potentially justifying a pause. Oil’s 1.81% drop on Ukraine peace hopes eased inflation fears, supporting lower yields, while gold’s 0.20% gain reflected safe-haven bids. EUR/USD slipped 0.18% amid DAX weakness, pressuring cross-asset flows. Overall, the yield dip reflects recalibrated Fed bets, but high valuations and G20 fissures—like US boycott over South Africa—keep volatility elevated, with upcoming retail sales pivotal for holiday spending amid tariff overhangs.