Summary:

Australian interest rates moved unevenly across the swap curves over the past week, reflecting mixed market sentiment around near-term funding conditions and longer-term policy expectations. Short-dated money-market maturities (1–6 months) experienced small upward pressure overall, while mid-to-long-dated yields (1–15 years) were generally slightly softer on the week but meaningfully higher over the month.

At the front end, the 1-month rate rose 4 bps to 3.55%, showing the strongest weekly increase, likely driven by tighter funding conditions and elevated rollover demand. The 3-month tenor inched up 1 bp to 3.64%, while the 6-month rate dipped 1 bp to 3.87%, suggesting stabilisation after earlier climbs. Over the month, however, all three short-term maturities recorded sizeable increases, ranging from 9 bps to 23 bps, reflecting persistent expectations that short-term liquidity and cash-rate pricing remain firm.

Across the swap/bond curve, yields softened modestly this week. The 1-year rate slipped 2 bps to 3.62%, while the 3-year fell 4 bps to 3.74%, indicating some easing in near-term policy expectations as markets reassess the timing of possible central-bank moves. The 5-year tenor declined 2 bps to 4.14%, consistent with a slight reduction in medium-term rate pressures.

Longer maturities were more stable. The 10-year rate edged up 2 bps to 4.52%, while the 15-year rose 1 bp to 4.73%, signalling minimal curve steepening over the week. Despite the small weekly shifts, all medium-to-long maturities are significantly higher over the past month, with gains of 30–41 bps. This reflects broader global repricing as bond markets incorporate higher-term premium assumptions and ongoing inflation uncertainty.

Overall, the curve shows a short-end firming, mid-curve softening, and long-end stability, with the month’s moves dominated by a clear upward shift in yields. Markets continue to balance Australia’s domestic rate outlook with global bond dynamics, producing a yield curve that remains upward sloping and sensitive to incoming economic signals.

Bank Bill Swap Rates

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 month 3.55 0.04 0.09 3 months 3.64 0.01 0.15 6 months 3.87 -0.01 0.23 SWAP RATES

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 year 3.62 -0.02 0.3 3 years 3.74 -0.04 0.39 5 years 4.14 -0.02 0.41 10 years 4.52 0.02 0.38 15 years 4.73 0.01 0.38 - Exhibit 1: Australian 3Y/10Y Bond Yield

-

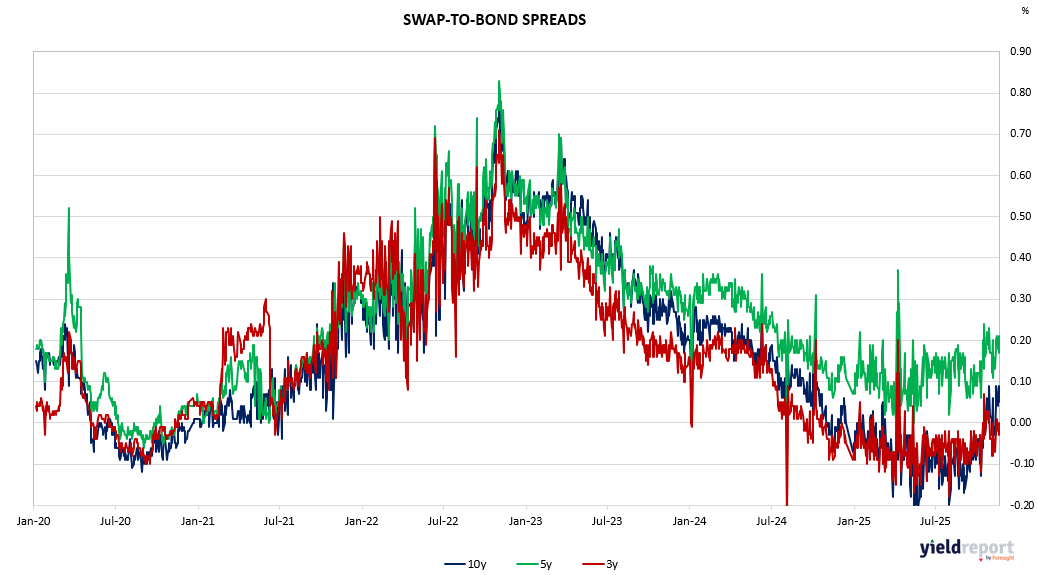

Swap-to-bond spread trends for 3-year, 5-year, and 10-year maturities, January 2020 to November 2025, with details on periods of volatility and trend toward zero

Swap-to-bond spread trends for 3-year, 5-year, and 10-year maturities, January 2020 to November 2025, with details on periods of volatility and trend toward zero