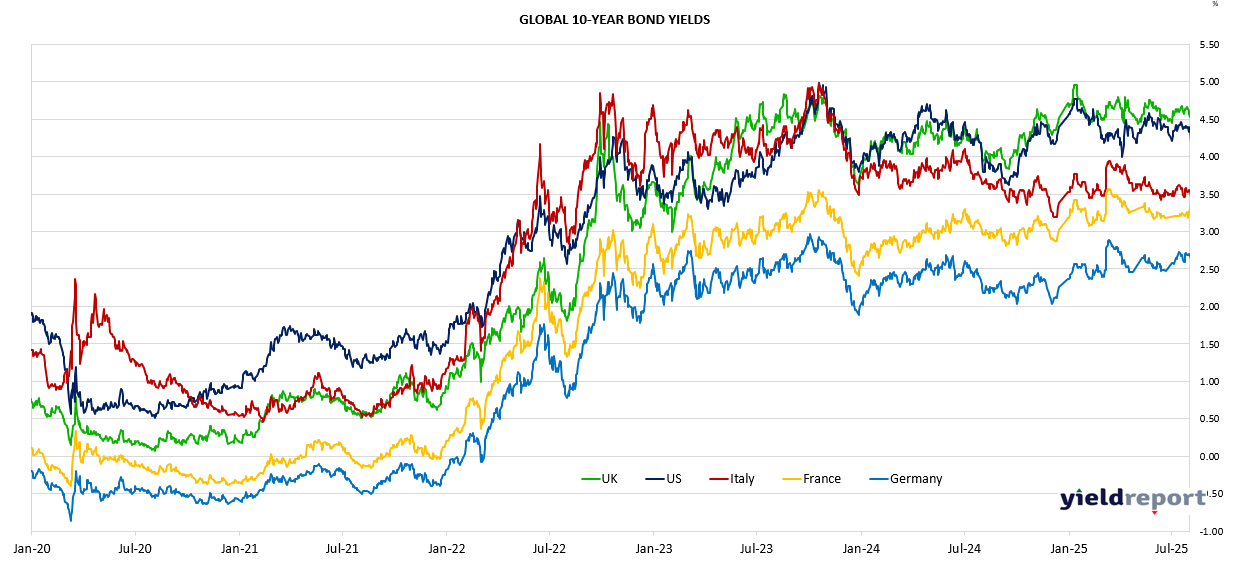

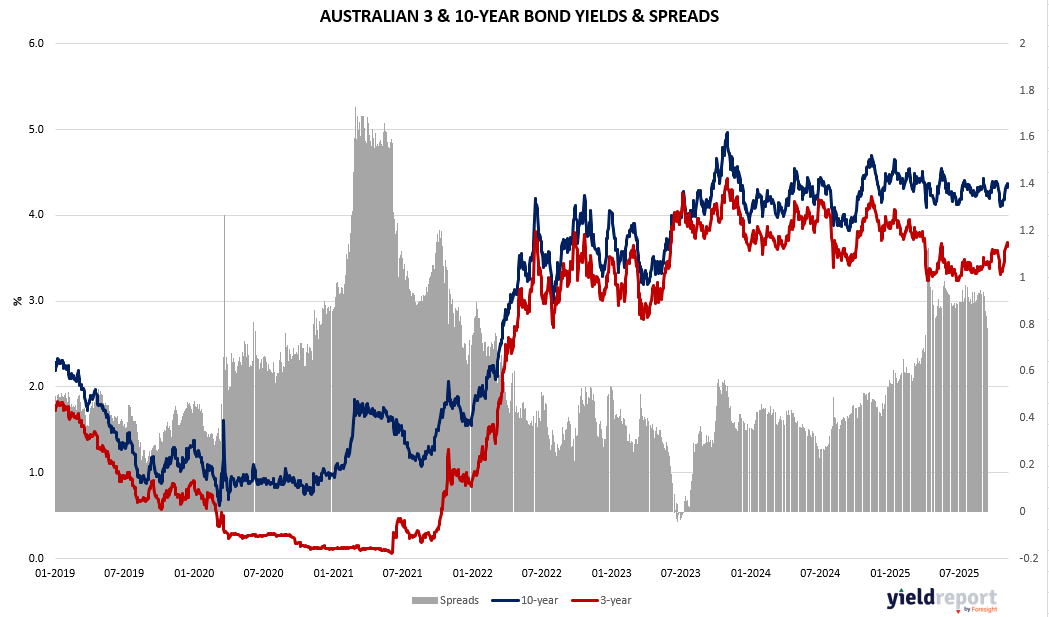

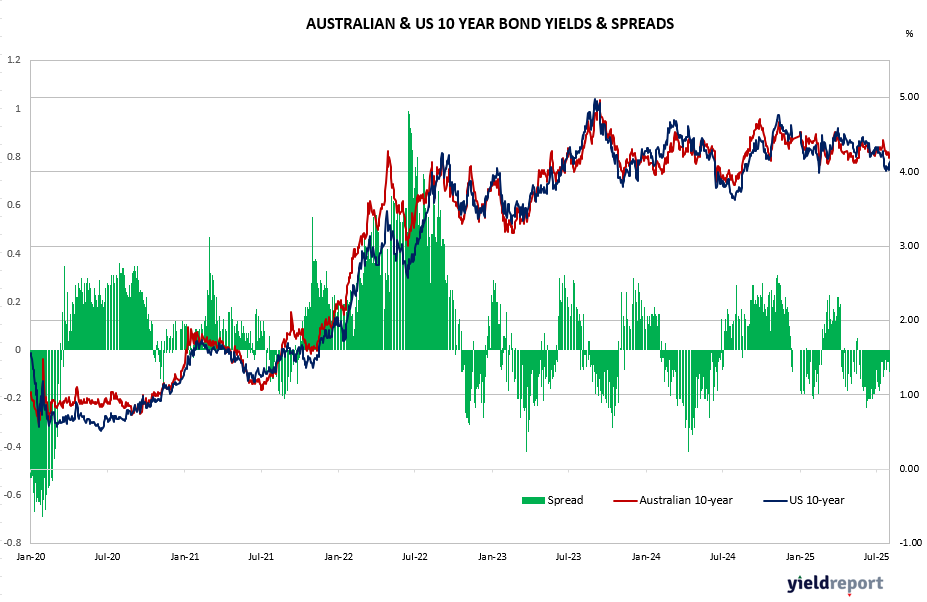

Summary:

Australian bond yields rose slightly over the week, with the 3-year up 3 basis points to 3.65%, the 10-year up 5bps to 4.36%, and the 30-year up 4bps to 4.99%. Short-term funding rates were steady, with the cash rate at 3.60% and the 3-month BBSW easing marginally to 3.64%. In the U.S., yields were mostly stable, with the 2-year down 4bps to 3.57%, the 10-year edging 1bp lower to 4.10%, and the 30-year up slightly to 4.70%. The Australian dollar weakened, falling 0.58% over the week to 64.81 US cents amid firmer global bond yields and renewed rate uncertainty.

Bond traders have largely abandoned expectations for further interest rate cuts by the Reserve Bank of Australia (RBA) after Governor Michele Bullock signalled that elevated inflation leaves the policy direction finely balanced. Speaking at a post-meeting press conference, Bullock said higher-than-expected inflation meant the next move could go “in either direction,” reinforcing the RBA’s data-dependent stance and dampening hopes for rate relief.

The Reserve Bank’s November forecasts reflect a less optimistic outlook after surprise rises in inflation and unemployment disrupted its near-perfect August projections. Headline inflation is expected to peak at 3.7% by mid-2026, with core inflation near 3%, both above the 2–3% target range. Temporary factors, including the February energy rebate roll-off, are driving short-term price spikes, though the RBA expects inflation to ease to about 2.6% later. The Bank concedes reduced economic capacity and higher inflation risks but left growth and unemployment forecasts largely unchanged. Markets have dropped expectations for further rate cuts, with attention now on upcoming CPI data.

The Australian Bond spreads (3 & 10 years) continue to indicate positive sloping yield curve with significant steepening in the curve occurring from July 2023 (phase 1) and then accelerating from July 2024. The current spread continues to be at cyclical highs although lower than record highs observed in2021. From an investment perspective, steepening yield curves and a rebounding lending environment are likely to boost domestic economic environment and bank profitability. In a similar vein, the spread between the US 2 year bonds and US 10 Year bond has also been steepening since July 2023.

Figure 1: Aust. 3 yr minus 10 yr Bond Spread

Figure 2: Australian & US Bond Yields

Figure 3: US 10-year minus 2-year Bond Spread